November 5, 2025

Which Infra Managers Are Generating Pure Alpha?

A new platform launched by Scientific Infra & Private Assets assesses just how much infra funds are outperforming the markets they operate in.

In Infrastructure Investor’s LP Perspectives survey released in February this year, one of the top concerns among LPs was performance issues. Specifically, 21 percent of investors reported that their infrastructure portfolios have underperformed benchmarks over the past year, the highest level since this survey began in 2018.

Yet the multitude of benchmarks being used and a lack of context behind them can often lead to further questions from LPs as to what is being measured and how well funds are actually performing.

Research group Scientific Infra & Private Assets (SIPA), formed out of the EDHEC Infrastructure & Private Assets Research Institute, believes it has the answer to some of these questions. Crucially, it is now assessing how much alpha is being delivered by infrastructure managers and funds, benchmarking against its Infra300 index, which tracks the monthly returns of 300 unlisted infrastructure companies and has a market capitalisation of $406.8 billion, as of September.

SIPA has now launched the Private Alpha platform, which uses the direct alpha model to rank infrastructure funds based on the alpha generated, as well as ranking GPs based on the collective scores of their respective funds.

“You take a fund, you have your cashflows in and out and your NAV, you adjust the cashflows to reflect the movement of the market index that you selected as your benchmark and then you recalculate the IRR,” Frederic Blanc-Brude, chief executive at SIPA, explained to Infrastructure Investor. “It’s an IRR which controls for or removes the effect of the market, as if part of the cashflows had been market returns. What you’re left with is direct alpha in the sense that it’s whatever IRR this fund generates that cannot be explained by the movements of the index that you’re using.”

Blanc-Brude said that SIPA gathered returns data from about 520 infrastructure funds amounting to circa $1.1 trillion of capital and about 800 buyout funds and measured against its respective indices for both asset classes.

“What we found in both infrastructure and private equity is that on average, the alpha is zero,” he revealed. “This is interesting because in every study of active equity managers, it’s always found that on average alpha is zero. The idea that we found zero was, for me, that this is the right index and we are looking at the right point of reference. About half of the funds beat the market and about half don’t, which makes sense.”

Two calculations factor into SIPA’s methodology, with one being the Infra300 index and another that takes into account the strategy of the fund in terms of the geographies and sectors it invests in.

For the Private Alpha platform, SIPA developed a Morning Star-esque ranking system, scoring funds and GPs on a five-starred basis alongside its alpha rating.

“If we have the alpha, we can easily back out the beta,” stated Blanc-Brude. “In other words, how much of the IRR of the fund is explained by the market and the exposure to market risk. If you have that, then we can also understand how much risk the fund is taking to generate this return. With some managers you win some, you lose some. Some managers tend to have positive alpha for all their funds, and some managers tend to have negative alpha fund after fund after fund. We can calculate the probability of outperformance, what you call alpha persistence.”

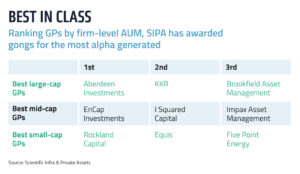

Meet the winners

SIPA has collated its findings to present GPs with awards for their efforts, categorising the GPs by large-cap, mid-cap and small-cap as defined by firm-level assets under management. That translates into Aberdeen Investments topping the large-cap list with a total alpha average of 9.49 percent across its funds, comparing fund performance with the broader market. Energy-focused managers EnCap Investments and Rockland Capital top the mid-cap and small-cap rankings, respectively, generating respective total alpha averages of 12.34 percent and 12.68 percent.

It also crowned individual funds split into categories such as Throwback Awards for realised funds, Midlife Awards for those still investing and a Green Shoot award for vintages from 2023. Equis Direct Investment Fund was crowned winner for the Throwback category, while ERA Infra Fund I and Peppertree Capital X were victorious in the Midlife and Green Shoot categories, respectively.

One fund performing exceptionally high in the rankings is the European renewables-focused Impax New Energy Investors IV, which closed on €439 million in May 2024. According to the Private Alpha platform, the fund is generating a 91.8 percent IRR, some 75.34 percent of which is driven by pure alpha. This is in part coming from an early capital gains focus, the manager said.

“The returns you see are probably reflective of some of the interim exits we’ve made,” said Casey Forester, head of private markets fundraising at Impax Asset Management. “To achieve these value-add returns, we’re taking development risk, taking it selectively across the portfolio, but we generally enter projects at an earlier stage working with developers and development platforms. As and when certain projects enter construction or reach COD, we look to sell those assets and recycle the capital back into our platform.”

The returns are also driven by taking an element of private equity risk in structuring some of the deals, according to Carsten Johansen, managing director at Impax. “We sit a bit in between the PE and infrastructure mentality. We need to grow a partnership with developers and that’s where the PE angle comes in, but our underwriting is probably more on the infrastructure downside case and making sure we get our capital back.

“In Europe we went through a period where you needed to have a government tariff. Then we had a period where PPAs became more prevalent and then a period where actually a lot of investors wanted merchant risk. Now, it’s a bit of an amalgamation. What we tend to do is before we start constructing an asset, we like to go to market and ask what the exit market is. It gets a certainty to an exit and reduces our downside. We like to lock in an exit before we commit our construction equity.”

Meanwhile, Jim Hughes, managing partner within EnCap’s energy transition team, explained the approach that’s led to its success. “For midstream and energy transition, our value-add is creating the assets. We’re not buyers of operating assets. We generally back management teams that have identified a market opportunity that may be a type of asset, a regional opportunity or market dislocation, but they’ve identified some market opportunity and we back a team that can execute. When you’re creating assets, it’s an execution game, it’s not financial engineering or market timing.

“It’s about discount rate compression. I can contract a yet-to-be-built solar or wind facility – the same is true of a gas processing plant or pipeline – at a return that is higher than the return it will be sold at when it is an operating asset. You get compensated for taking the construction risk and end up with a significant capital gain. We’ve delivered closer to private equity returns, but we do so against an infrastructure asset class by taking that very specific risk.”

The winners of the awards will be presented at an event in New York on 22 October.

Download the original article here.